Global aviation manufacturing represents one of the world’s most strategically important and technologically advanced industries, with only a handful of nations possessing the industrial capacity, technical expertise, and capital resources to design and produce modern aircraft at scale. The question of which country builds the most aircraft reveals fascinating insights into economic power, military capabilities, and industrial competitiveness across commercial aviation, defense systems, and business jet markets.

The United States maintains its position as the world’s leading aircraft manufacturing nation in 2026, producing more total aircraft than any other country when combining commercial airliners, military jets, business aircraft, and general aviation planes. However, Europe through Airbus challenges American dominance in commercial aviation specifically, while China emerges as an increasingly significant player with ambitious manufacturing programs targeting both domestic and international markets.

This comprehensive analysis examines aircraft manufacturing by country across all major categories, explaining why certain nations dominate specific segments, how production volumes compare between the United States, Europe, China, and other manufacturers, and what challenges and opportunities shape the future of global aviation manufacturing. Understanding which countries produce the most aircraft illuminates broader questions about industrial capability, technological leadership, and economic competitiveness in the 21st century aerospace sector.

Which Country Builds the Most Aircraft in 2026?

The United States produces the most aircraft globally in 2026 when measuring total aircraft production across all categories including commercial jets, military aircraft, business jets, and general aviation planes. American manufacturers collectively deliver approximately 2,000-2,500 aircraft annually across these segments, maintaining the nation’s century-long position as the world’s preeminent aviation manufacturing power.

This leadership position reflects the United States’ dominance in multiple aircraft categories simultaneously. While Europe through Airbus matches or slightly exceeds Boeing in commercial aircraft deliveries specifically, American manufacturers overwhelmingly lead in military aircraft production through companies like Lockheed Martin, Northrop Grumman, and Boeing Defense, in business aviation through Gulfstream and Textron, and in general aviation through Cessna, Cirrus, and Piper. No other country competes across all these segments with equivalent scale and technological sophistication.

Measuring which country produces the most airplanes requires defining metrics carefully. Commercial aircraft deliveries show near parity between the United States (Boeing) and Europe (Airbus), with each delivering 450-550 commercial jets annually. However, when adding military aircraft (where the U.S. produces 200-300+ annually versus minimal European commercial military production), business jets (U.S. produces 600-800 annually versus negligible European production), and general aviation aircraft (U.S. produces 1,000+ annually), American total aircraft production substantially exceeds any individual country or regional bloc.

China represents the fastest-growing aircraft manufacturing nation, with domestic production increasing as COMAC’s C919 enters commercial service and military aircraft manufacturing expands. However, Chinese total aircraft production remains substantially below American and European levels in 2026, with manufacturers delivering approximately 100-200 commercial and military aircraft combined as indigenous programs mature and production rates gradually increase.

Top Aircraft Manufacturing Countries in 2026

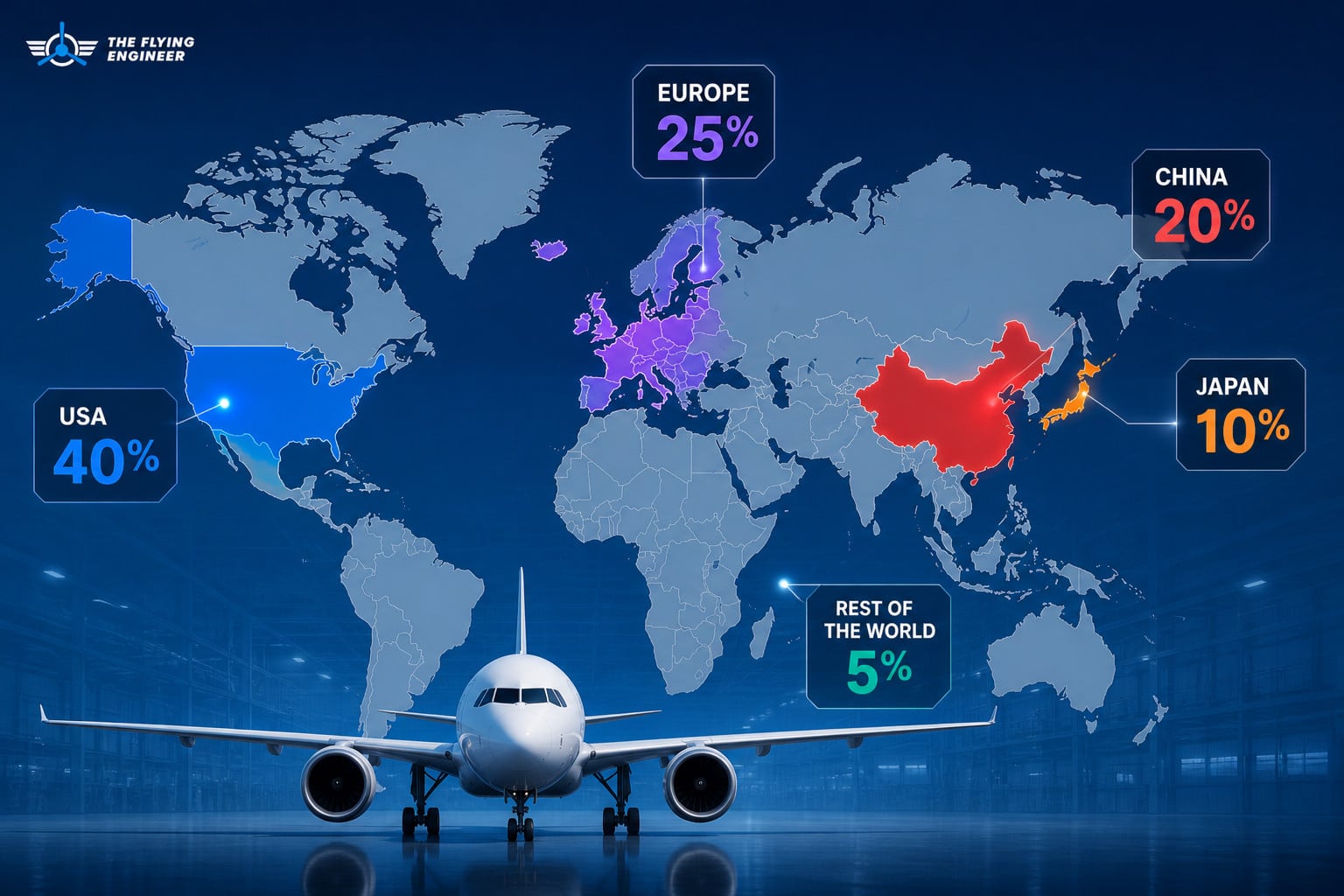

The global aviation manufacturing landscape concentrates production among a small number of technologically advanced nations with the industrial base, engineering talent, and capital resources required to design and build modern aircraft. Five countries and regional blocs account for over 95% of global aircraft production by value and volume, with the United States, Europe, China, Canada, and Brazil representing the industry’s core manufacturing centers.

United States – The Global Leader

The United States maintains unchallenged leadership in total aircraft production through a diverse ecosystem of manufacturers spanning commercial aviation, military systems, business jets, and general aviation. Boeing represents America’s commercial aviation flagship, delivering approximately 450-500 commercial aircraft annually from facilities in Renton (737 family), Everett (767, 777), and North Charleston (787). Despite recent challenges including 737 MAX grounding and pandemic disruption, Boeing remains one of only two manufacturers globally capable of producing large commercial aircraft at scale.

American military aircraft production dwarfs all competitors, with the United States accounting for roughly 50-60% of global military aircraft manufacturing by value. Lockheed Martin produces F-35 Lightning II fighters at rates approaching 150-180 aircraft annually across Fort Worth and other facilities, serving U.S. military branches and international customers through the world’s largest fighter program. Northrop Grumman manufactures B-21 Raider bombers and advanced military aircraft, while Boeing Defense produces F-15EX fighters, F/A-18 Super Hornets, and military derivatives of commercial platforms.

The business jet sector showcases another area of overwhelming American dominance. Gulfstream (a General Dynamics subsidiary) delivers 130-150 large-cabin business jets annually from Savannah, Georgia, representing the premium segment of corporate aviation. Textron Aviation through its Cessna and Beechcraft brands produces 250-350 business jets and turboprops annually, spanning from entry-level Citation jets to King Air turboprops. Bombardier (Canadian-owned) manufactures Learjet and Challenger aircraft in the United States, further reinforcing American production capacity.

General aviation represents perhaps America’s most dominant aircraft manufacturing segment, with U.S. companies producing over 1,000 piston and light aircraft annually. Textron Aviation’s Cessna produces the world’s most popular single-engine aircraft including the Skyhawk and TTx. Cirrus Aircraft delivers 300-400 SR-series aircraft annually, pioneering safety innovations including whole-aircraft parachutes. This general aviation ecosystem, largely absent in other countries, significantly boosts total U.S. aircraft production numbers.

France & Europe – Airbus Powerhouse

Europe challenges American aviation manufacturing leadership through Airbus, the continent’s multinational aircraft manufacturing consortium headquartered in Toulouse, France, with major production facilities across France, Germany, Spain, and the United Kingdom. Airbus delivers approximately 500-550 commercial aircraft annually, slightly exceeding Boeing’s recent delivery rates and capturing roughly 55% of the global commercial aircraft market by orders in recent years.

The A320neo family represents Airbus’s commercial aviation crown jewel, with the manufacturer producing these narrowbody jets at facilities in Toulouse, Hamburg, Mobile (Alabama), and Tianjin (China) at combined rates approaching 50-60 aircraft monthly. The A320neo, A321neo, and A321XLR variants dominate the single-aisle market, outselling Boeing’s 737 MAX family in most recent order competitions. Airbus’s widebody production includes the A350 XWB and A330neo, both competitive products serving long-haul markets globally.

European aircraft manufacturing operates through a unique collaborative model reflecting the continent’s political and industrial structure. Airbus itself represents a multinational consortium with French, German, Spanish, and British participation, with final assembly occurring in multiple countries and component manufacturing distributed across dozens of European sites. This model creates political resilience and industrial diversification but introduces coordination complexities absent in American manufacturers’ more centralized operations.

Europe’s aircraft manufacturing concentrates almost entirely on commercial aviation through Airbus, with minimal military aircraft, business jet, or general aviation production compared to American industry breadth. European military aircraft programs like the Eurofighter Typhoon involve multiple nations but produce relatively small numbers (20-40 annually across all participating countries). European business jet manufacturing barely registers compared to American dominance, while general aviation remains a negligible European industry sector.

China – The Rising Challenger

China represents global aviation manufacturing’s most significant emerging force, with the country investing tens of billions of dollars developing indigenous aircraft manufacturing capabilities targeting both domestic market demand and eventual international competitiveness. The Commercial Aircraft Corporation of China (COMAC) leads Chinese commercial aviation efforts, with the C919 narrowbody jet entering commercial service in 2023 and gradually ramping production toward planned rates of 150 aircraft annually by the late 2020s.

The C919 competes directly with the Boeing 737 and Airbus A320 families, designed to serve China’s massive domestic aviation market where over 1,000 narrowbody aircraft operate and hundreds more are needed annually to support growth. Early C919 production remains limited to 20-40 aircraft annually as COMAC addresses certification requirements, establishes manufacturing processes, and develops supply chain reliability. However, Chinese government support ensures continued investment regardless of near-term economic returns, positioning COMAC for long-term competition.

Chinese military aircraft manufacturing represents a substantial but less transparent industry segment. State-owned Aviation Industry Corporation of China (AVIC) produces J-20 fifth-generation fighters, J-10 and J-11 fighter variants, Y-20 strategic transports, and numerous other military aircraft types. Estimated Chinese military aircraft production ranges from 100-150 aircraft annually, supporting People’s Liberation Army modernization programs and replacing aging Soviet-era equipment throughout China’s massive military aviation fleet.

China’s aviation manufacturing strategy prioritizes domestic market capture before international expansion, with government policies requiring Chinese airlines to purchase domestically-produced aircraft when available. This guaranteed domestic demand provides COMAC and other Chinese manufacturers with production volumes supporting manufacturing learning curves and technology development, even without international commercial success. Whether Chinese manufacturers can achieve the quality, reliability, and after-sales support required for global competitiveness remains uncertain, but China’s determination to develop indigenous capabilities appears unwavering.

Russia – Military Strength, Commercial Struggles

Russia maintains significant military aircraft manufacturing capabilities inherited from Soviet-era industrial programs, with manufacturers producing 50-80 military aircraft annually including Su-35 and Su-57 fighters, attack helicopters, and transport aircraft. However, Russian commercial aircraft manufacturing largely collapsed following the Soviet Union’s dissolution, with United Aircraft Corporation producing minimal numbers of Sukhoi Superjet 100 regional jets and essentially no widebody commercial aircraft competitive with Western manufacturers.

Western sanctions following Russia’s 2022 invasion of Ukraine severely disrupted Russian aviation manufacturing, cutting access to critical components including engines, avionics, and composite materials previously imported from Europe and the United States. This forced Russia to substitute inferior domestic alternatives or source components from China, degrading aircraft performance and reliability. International commercial aircraft sales effectively ceased as Western nations prohibited exports to Russia and Russian manufacturers lost access to certification and support networks.

Canada & Brazil – Regional Aircraft Leaders

Canada and Brazil occupy specialized niches in global aviation manufacturing, focusing on regional jets and specialized aircraft rather than competing directly with Boeing and Airbus in large commercial aircraft. Bombardier (Canadian) historically manufactured C-Series aircraft before selling the program to Airbus (now A220), and continues producing business jets through its Global and Challenger families. The company delivers 120-150 business jets annually, competing with American manufacturers in the premium corporate aviation segment.

Brazil’s Embraer represents the world’s third-largest commercial aircraft manufacturer, specializing in regional jets seating 70-150 passengers. The company’s E-Jet E2 family competes with Airbus’s A220 and serves airlines requiring smaller aircraft than Boeing or Airbus narrowbodies. Embraer delivers 80-120 commercial and business aircraft annually from Brazilian facilities, maintaining technological competitiveness despite dramatically smaller scale than Boeing or Airbus.

Aircraft Production by Category

Understanding aircraft production statistics by country requires examining different aircraft categories separately, as national strengths vary significantly across commercial aviation, military systems, business jets, and general aviation. Total production leadership depends partly on which categories are weighted most heavily in comparative analysis.

Commercial Aircraft Production (2026 Annual Deliveries):

- United States (Boeing): 450-500 aircraft annually, including 737 MAX family, 787 Dreamliner, 777, and 767 variants across narrowbody and widebody segments

- Europe (Airbus): 500-550 aircraft annually, including A320neo family, A330neo, and A350 across the manufacturer’s narrowbody and widebody product lines

- China (COMAC): 20-40 C919 aircraft annually in early production ramp-up phase, targeting 150+ annually by late 2020s

- Canada (Bombardier via Airbus A220): Production now counted under Airbus following program sale, with A220 contributing 50-70 annual deliveries

- Brazil (Embraer): 60-80 commercial jets annually, primarily E-Jet E2 regional aircraft serving 70-150 seat market segment

Military Aircraft Production (2026 Estimates):

- United States: 200-300+ military aircraft annually, including F-35 fighters (~150-180), F-15EX, F/A-18, strategic bombers, transport aircraft, and helicopters across multiple manufacturers

- China: 100-150 military aircraft annually (estimated), including J-20, J-10, J-11 fighters, Y-20 transports, and various helicopter and trainer aircraft

- Russia: 50-80 military aircraft annually, including Su-35, Su-57 fighters, attack helicopters, though production affected by sanctions and component access

- Europe: 30-50 military aircraft annually across multiple countries, including Eurofighter Typhoon, Rafale, and various transport/support aircraft

- Other nations: Limited indigenous production, primarily licensed manufacturing of foreign designs or small-scale programs serving domestic defense needs

Business Jet Production (2026 Deliveries):

- United States: 600-800 business jets annually, dominated by Gulfstream (130-150), Textron Aviation/Cessna (250-350), and Bombardier U.S. facilities

- Canada (Bombardier): 120-150 business jets annually across Global and Challenger families, though many manufactured in U.S. facilities

- Brazil (Embraer): 20-30 business jets annually through Phenom and Praetor families, smaller scale than North American competitors

- Europe: Minimal business jet production, primarily limited to Dassault Falcon jets from France (30-40 annually)

General Aviation Production (2026 Estimates):

- United States: 1,000+ general aviation aircraft annually, including Cessna single-engines, Cirrus SR-series, Piper aircraft, and numerous smaller manufacturers

- Other countries: Minimal general aviation production compared to American dominance, with most international general aviation aircraft being American imports

| Country/Region | Major Companies | Primary Strength Area | Annual Production (Est.) |

|---|---|---|---|

| United States | Boeing, Lockheed Martin, Northrop Grumman, Gulfstream, Textron/Cessna | All categories: Commercial, military, business jets, general aviation | 2,000-2,500 aircraft |

| France/Europe | Airbus (multinational consortium) | Commercial aircraft (narrowbody and widebody) | 500-550 commercial aircraft |

| China | COMAC, AVIC (Aviation Industry Corporation) | Emerging commercial, established military | 120-200 total aircraft |

| Canada | Bombardier (business jets) | Business jets, formerly regional aircraft | 120-150 business jets |

| Brazil | Embraer | Regional commercial jets, business jets | 80-120 total aircraft |

| Russia | United Aircraft Corporation, Sukhoi | Military aircraft, limited commercial | 50-80 military aircraft |

Note: Production figures represent approximate annual totals across all aircraft categories. U.S. figure includes commercial, military, business, and general aviation; other countries primarily commercial and/or military.

Boeing vs Airbus – Which Country Benefits More?

The Boeing versus Airbus competition represents more than corporate rivalry between two aircraft manufacturers. It reflects broader economic competition between the United States and Europe, with each manufacturer generating hundreds of thousands of jobs, billions in exports, and substantial industrial capability benefiting their respective home regions. Determining which country or region benefits more from their champion manufacturer involves examining employment, exports, supply chain economics, and strategic industrial capabilities.

Boeing directly employs approximately 170,000-180,000 workers globally, with roughly 130,000-140,000 based in the United States concentrated in Washington, South Carolina, California, and other states hosting major facilities. The company’s U.S. supply chain involves thousands of suppliers across all 50 states, supporting an estimated 1.5-2 million additional jobs through direct and indirect economic activity. Boeing ranks among America’s largest exporters, generating $60-80 billion annually in revenue with significant portions from international sales supporting the U.S. trade balance.

Airbus distributes economic benefits across multiple European nations reflecting its multinational structure. The company employs approximately 130,000-140,000 workers across Europe, with major concentrations in France (50,000+), Germany (40,000+), Spain (10,000+), and the United Kingdom (15,000+). Airbus’s supply chain spans European industrial capabilities, with wings manufactured in Britain, fuselage sections in Germany, and final assembly in France and Germany. This distribution creates political support across multiple countries, though it also introduces coordination costs and inefficiencies compared to Boeing’s more centralized American operations.

From an economic impact perspective, both Boeing and Airbus generate roughly comparable employment and economic activity, though measured differently due to Airbus’s multinational structure versus Boeing’s concentrated American presence. The United States arguably captures more unified national benefit from Boeing than any single European country captures from Airbus, though Europe collectively benefits from Airbus employment and industrial capability distributed across the continent.

The strategic industrial capability represented by commercial aircraft manufacturing transcends pure economics. Both Boeing and Airbus provide their home regions with design expertise, manufacturing capabilities, and supply chain depth supporting not only commercial aviation but also military aircraft, space systems, and broader aerospace technologies. This industrial base proves difficult to replicate, helping explain government support for both manufacturers through various mechanisms including research funding, export financing, and regulatory assistance.

Why the US Still Leads Global Aircraft Production

The United States maintains its position as the world’s leading aircraft manufacturing nation despite intense European competition through Airbus and China’s rapid industrial development. This enduring American leadership reflects multiple reinforcing advantages spanning defense spending, industrial ecosystems, technological innovation, market scale, and institutional capabilities accumulated over decades of aviation industry development.

Defense spending represents perhaps the most significant factor sustaining American aircraft manufacturing leadership. The United States spends over $800 billion annually on defense, with substantial portions funding aircraft procurement and aerospace research. This military demand supports manufacturers including Lockheed Martin, Northrop Grumman, and Boeing Defense that have minimal or no international equivalents at comparable scale. Military programs provide stable revenue streams enabling manufacturers to maintain engineering talent, production facilities, and supply chains benefiting both military and commercial operations.

The American aerospace industrial ecosystem creates compound advantages difficult for other countries to replicate. Hundreds of specialized suppliers, engineering firms, testing facilities, certification authorities, and research institutions concentrate in clusters around major manufacturers, creating knowledge spillovers, labor markets, and innovation networks. This ecosystem depth means new aerospace ventures in the United States can access capabilities and expertise unavailable in countries with less developed aerospace sectors, reinforcing American competitive advantages across successive technology generations.

Technological innovation leadership perpetuates American aviation manufacturing dominance across commercial, military, and business aviation. U.S. manufacturers pioneered jet engines, fly-by-wire controls, composite airframes, and numerous other technologies defining modern aircraft. This innovation leadership reflects substantial research and development spending (Boeing invests $3-4 billion annually in R&D), university research programs (MIT, Georgia Tech, others), and government funding through NASA, DARPA, and military research organizations. The resulting technological edge helps American manufacturers compete despite higher labor costs than emerging competitors.

Market scale and domestic demand provide American manufacturers with advantages supporting global competitiveness. The United States represents the world’s largest aviation market by passenger traffic and commercial aircraft fleet size, providing Boeing with substantial domestic orders supporting production rates and manufacturing efficiency. American airlines’ historic preference for Boeing aircraft (though declining versus Airbus in recent years) provides the manufacturer with anchor customers facilitating program launches and production stability even during international sales challenges.

Institutional capabilities accumulated over a century of aircraft manufacturing create less visible but important American advantages. The Federal Aviation Administration’s certification processes, though sometimes criticized, establish global gold standards other regulators reference. American aerospace engineering education produces thousands of qualified graduates annually from institutions with decades of aerospace focus. Financial markets understand aerospace industry economics and provide capital for development programs. These institutional capabilities prove difficult for emerging aerospace nations to replicate regardless of government investment levels.

Challenges Facing Aircraft Manufacturing Countries

All major aircraft manufacturing nations confront significant operational and strategic challenges in 2026, with supply chain disruptions, labor shortages, certification delays, and geopolitical tensions affecting production across the United States, Europe, China, and other producers. These industry-wide pressures test manufacturers’ resilience and countries’ ability to maintain competitive positions as market conditions evolve and new competitors emerge.

Supply chain constraints represent the most immediate challenge limiting aircraft production across all major manufacturing nations. Critical component shortages including engines (Pratt & Whitney GTF issues particularly acute), avionics systems, landing gear, and specialized fasteners force production delays and complicate delivery schedules. These shortages reflect pandemic-related disruptions, supplier capacity limitations, and increased demand as airlines accelerate fleet modernization programs. Neither American nor European manufacturers can significantly increase production without corresponding supplier capacity expansion requiring time and capital investment.

Labor shortages affect aircraft manufacturing globally as companies struggle to recruit and retain skilled aerospace workers including mechanics, engineers, and quality inspectors. The United States faces particular challenges as experienced aerospace workers retire and younger workers show less interest in manufacturing careers compared to software and other technology sectors. European manufacturers confront similar demographic trends, while Chinese aerospace industry growth outpaces workforce development creating quality control concerns. Training new aerospace workers to required skill levels requires months or years, limiting how quickly manufacturers can expand production regardless of demand levels.

Certification delays plague specific aircraft programs, most notably Boeing’s 737 MAX 10 and 777-9 facing extended regulatory review timelines. Regulatory authorities including the FAA maintain heightened scrutiny following 737 MAX accidents, extending approval processes and creating uncertainty for manufacturers and airline customers. These delays particularly affect American manufacturers given Boeing’s larger number of pending certifications, though all manufacturers face increasingly rigorous certification requirements as regulators prioritize safety over approval speed.

Geopolitical tensions increasingly disrupt aircraft manufacturing and sales, with U.S.-China technology restrictions limiting component access, Russian sanctions disrupting supply chains, and various trade disputes affecting international cooperation. These tensions force manufacturers to navigate complex export controls, diversify supply chains away from geopolitically vulnerable sources, and manage customer relationships amid government pressure. Aircraft manufacturing’s inherently global nature makes the industry particularly vulnerable to rising nationalism and great power competition fragmenting previously integrated international markets.

Sustainability requirements present longer-term challenges requiring substantial technological development and capital investment. Governments worldwide mandate emissions reductions, with aviation industry facing pressure to adopt sustainable aviation fuel, develop electric or hydrogen propulsion, and improve aircraft efficiency beyond current technology trajectories. These requirements may advantage manufacturers with greater research capabilities and capital resources (favoring established American and European companies) while creating barriers for emerging competitors lacking resources for expensive clean technology development.

Future of Global Aircraft Manufacturing

The future of global aircraft manufacturing will likely see continued American leadership across total production, European strength in commercial aviation through Airbus, and gradual Chinese market share gains as COMAC and other manufacturers mature. However, several trends may reshape competitive dynamics including sustainability requirements, supply chain reconfiguration, emerging technologies, and geopolitical fragmentation potentially creating opportunities for new entrants or disrupting established manufacturers.

China represents the most significant wildcard in aviation manufacturing’s future. If COMAC successfully achieves its production and quality targets, China could become the world’s third major commercial aircraft manufacturer within the next decade, initially serving primarily domestic markets before potentially competing internationally. Chinese military aircraft production will almost certainly grow as the country continues military modernization programs. However, whether Chinese manufacturers can achieve the reliability, safety records, and customer support necessary for sustained global competitiveness remains uncertain given limited operational history and persistent quality concerns.

Sustainability mandates may reshape competitive dynamics by requiring technologies and capabilities distributed unevenly among manufacturers and countries. If hydrogen or electric propulsion eventually becomes mandatory for certain aircraft categories, manufacturers with advanced research programs and capital resources may gain advantages over competitors lacking these capabilities. Conversely, emerging propulsion technologies could create opportunities for new entrants disrupting established manufacturers if technology shifts prove sufficiently radical.

Supply chain reconfiguration driven by pandemic lessons and geopolitical concerns may benefit countries and regions with more complete domestic aerospace ecosystems. The United States and Europe both possess relatively comprehensive supply chains compared to China’s dependence on imported engines and avionics. However, rising labor costs in developed nations create ongoing pressure to offshore production, with aircraft manufacturers continuously balancing supply chain resilience against cost optimization in component sourcing decisions.

New aircraft categories including urban air mobility vehicles, autonomous aircraft, and specialized logistics drones may create opportunities for countries and manufacturers currently lacking commercial aircraft capabilities. If these emerging categories prove commercially significant, nations including South Korea, Japan, and others with strong aerospace components industries but limited aircraft assembly experience might develop meaningful production capabilities in next-generation aviation segments.

Conclusion: America Leads, but Competition Intensifies

The United States maintains clear leadership as the country building the most aircraft in 2026, with American manufacturers collectively producing approximately 2,000-2,500 aircraft annually across commercial, military, business, and general aviation categories. This total production substantially exceeds any competitor when measured comprehensively, though Europe through Airbus matches or exceeds American commercial aircraft production specifically.

American aviation manufacturing leadership reflects dominance across multiple aircraft categories rather than narrow specialization in one segment. While Boeing and Airbus compete roughly evenly in commercial aviation, the United States overwhelmingly leads in military aircraft through Lockheed Martin and Northrop Grumman, in business jets through Gulfstream and Textron, and in general aviation through Cessna and Cirrus. This diversified production base provides resilience and ensures continued American leadership even as specific segments face competitive pressure.

Europe represents America’s primary competitor through Airbus, which leads in commercial aircraft orders and matches Boeing in deliveries while generating comparable economic benefits across multiple European nations. However, Europe’s concentration on commercial aviation limits total aircraft production compared to America’s broader manufacturing base. China emerges as aviation manufacturing’s most significant rising power, though whether Chinese manufacturers can achieve quality and reliability standards required for global competitiveness remains uncertain.

Looking ahead, American aircraft manufacturing leadership appears sustainable through the 2020s barring major disruptions, supported by defense spending, technological advantages, and industrial ecosystem depth. However, competition will intensify as Airbus continues commercial aviation success, China develops indigenous capabilities, and sustainability requirements potentially reshape competitive dynamics. The question of which country builds the most aircraft may have a clear answer in 2026, but the aviation manufacturing landscape continues evolving as new technologies, markets, and competitors challenge established hierarchies.